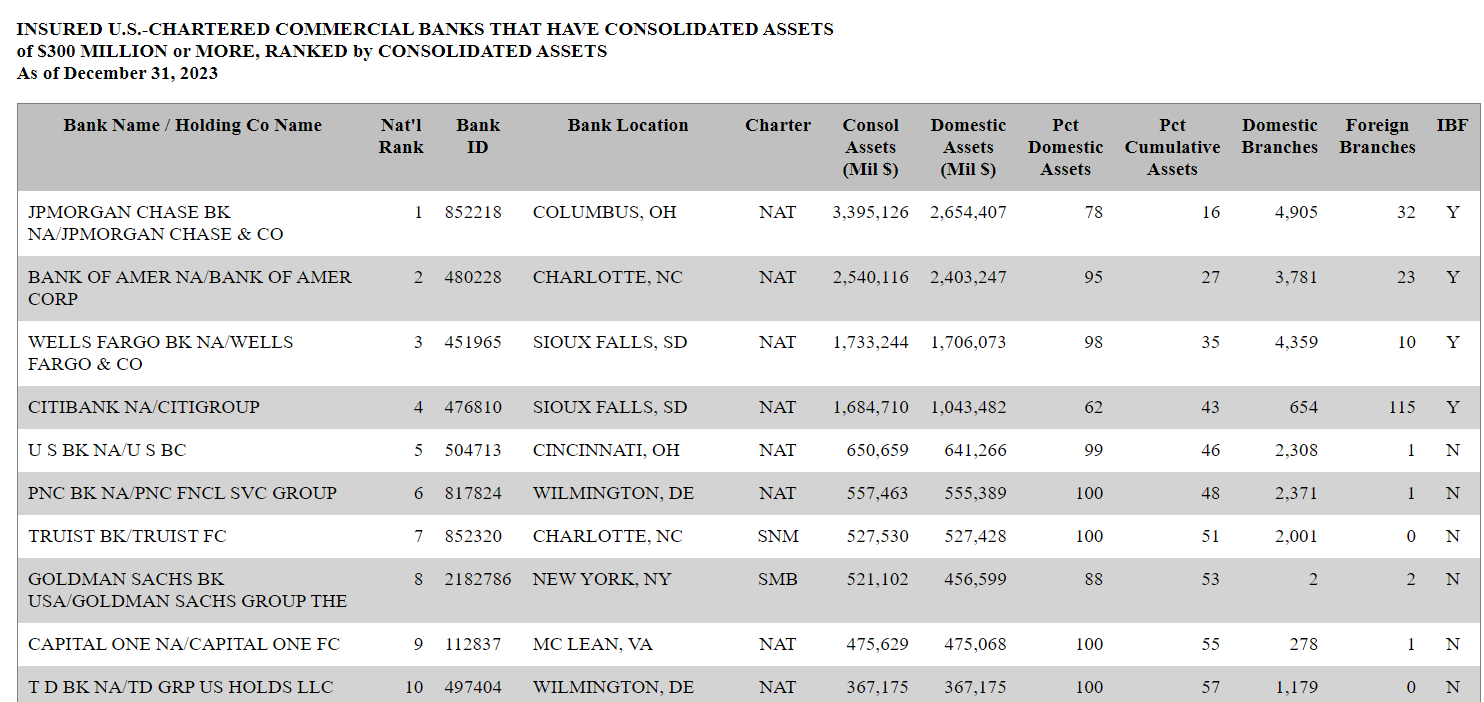

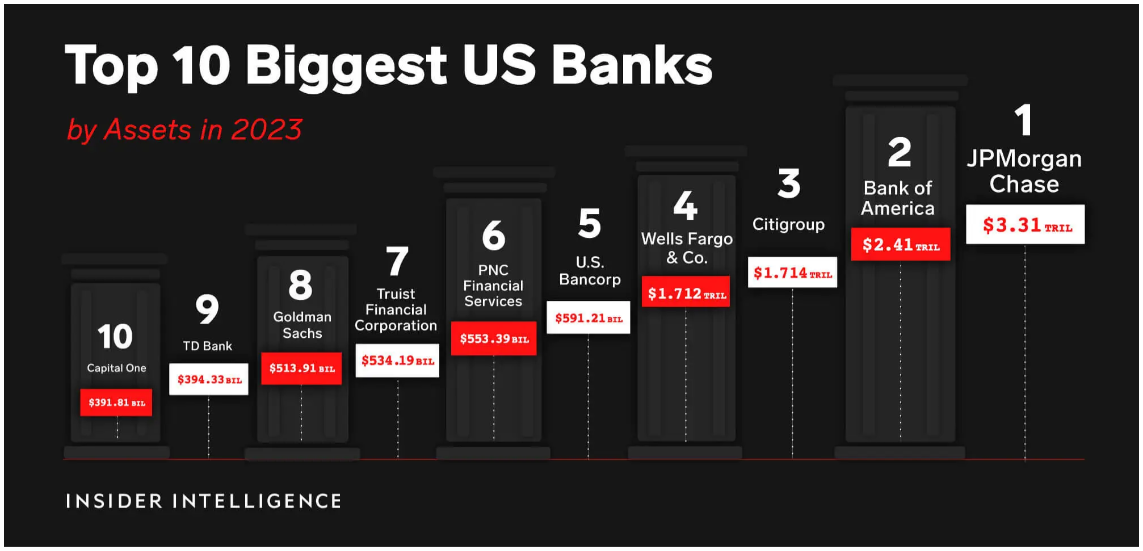

Last year we published the list of the top 10 US banks by consolidated assets at the end of 2022 / start of 2023. Find the blog here. It is interesting what a difference a year makes. While the top 10 is constituted by the same banks, TD Bank was dethroned from the Number 9 position by Capital One. The top 10 US Banks by consolidated assets at the end of 2023 / start of 2024 according to US Federal Reserve data are:

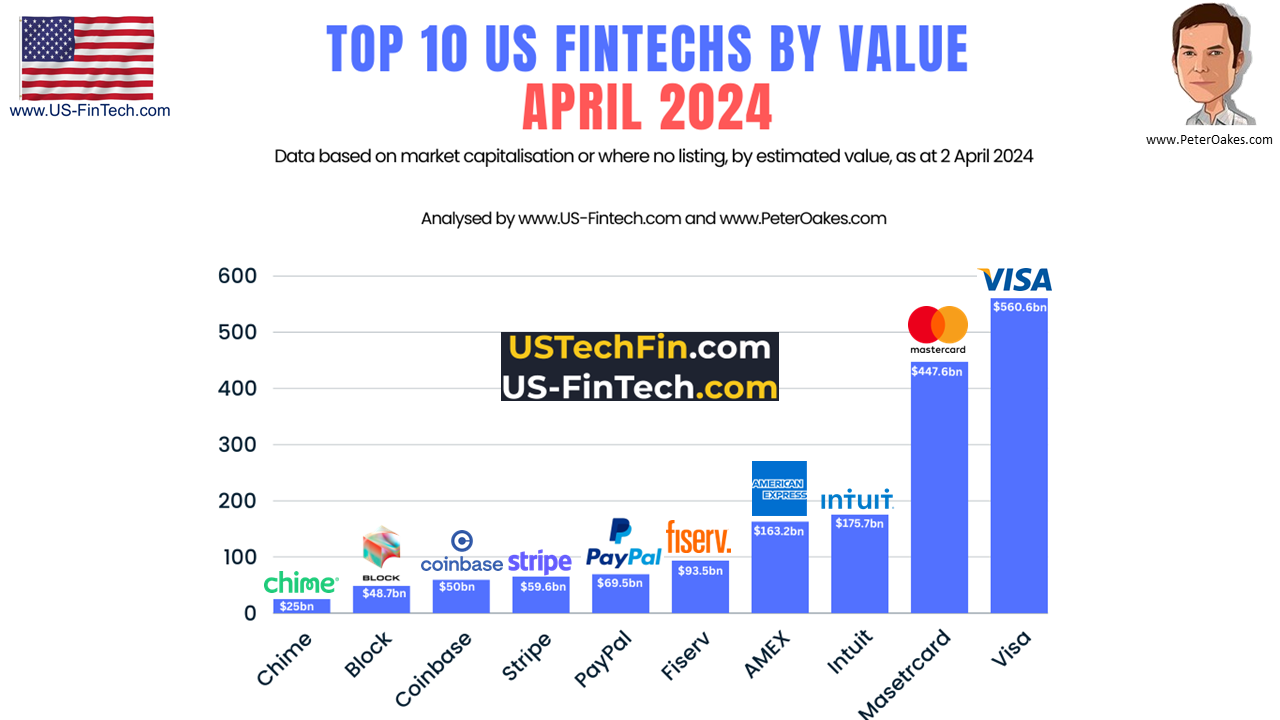

The top 10 #USfintech by market cap / estimated value (as of today - 02 April 2024) are:

One thought - With the top 5 US Banks being 4 times larger than the next 5 and those 2nd tier 5 banks having total assets 1.4 times greater than the market capitalisation / estimated value of the top 10 US fintech companies: "How can small(er) incumbent banks compete with both these existing giants and the continual onslaught of neobanks, challenger banks and non-banks offering banking services"? My tally of US banks is 2,140 banks (i.e. insured US-Chartered Commercial Banks with consolidated assets of $300mn or more). Source: (1) Peter Oakes and (2) https://www.federalreserve.gov/releases/lbr/current/default.htm

Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland) #FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com

0 Comments

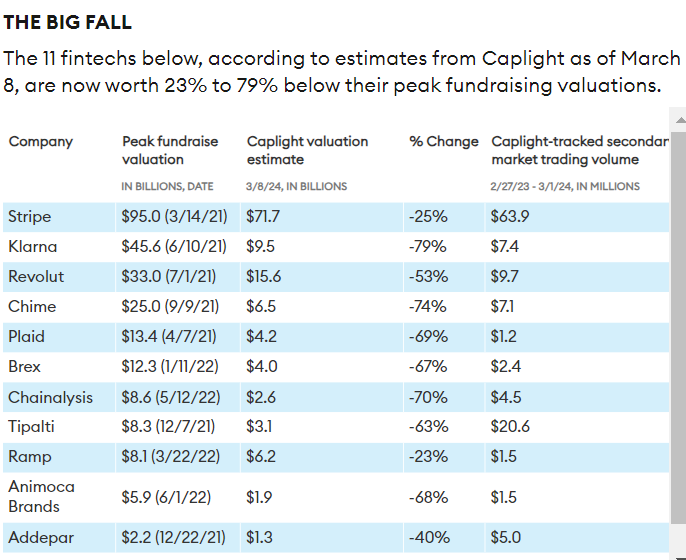

The current estimated value of 11 leading private fintech startups shows declines as high as 79%. But a few have started to recover. Back in November 2021, as the market for venture capital funding of fintech companies was peaking, San Francisco Bay Area bill-payment startup Tipalti raised $270 million at an $8.3 billion valuation. Then last summer, shares in the company traded hands privately at a $4 billion value. Today, by one estimate, Tipalti is worth just $3.1 billion, down 63% from its peak, even though it has been growing smartly—to 3,500 mostly U.S.-based business customers now, up from 2,000 at the end of 2021. Chen Amit, Tipalti’s 58-year-old Israeli cofounder and CEO, considers $3 billion way too low, but he acknowledges that the inflated valuations of 2021 are history. “We just need to accept it. There's no need to fight it,” Amit says, pointing to other private fintech companies, such as Stripe and Klarna, that have raised money since then in down rounds. He adds: “I will not sell my shares at $3 billion. I doubt any knowledgeable person would.” The extraordinary boom and bust in venture capital funding for the fintech industry has left a puzzle in its wake: what are these startups really worth today? With VC dollars flowing to the industry plunging from $141 billion in 2021 to $39 billion globally in 2023, according to CB Insights, many startups have scrambled to conserve cash to avoid raising funds at a dramatically reduced valuation. Meanwhile, those further along the growth path have delayed initial public offerings as already-public fintechs are languishing, off about 50% from their peak, despite the S&P 500 and the tech-heavy Nasdaq recently setting new highs. All that has left a void of information—one now being filled by new platforms like Caplight and Notice that generate valuation estimates based on the secondary-market trades they track through their partnerships with brokers. These estimates may also incorporate public disclosures of markdowns taken by mutual funds holding shares in private companies, the prices of comparable publicly traded stocks and other data. Soon after Tipalti’s 2021 fundraise, stocks started tanking and the Federal Reserve began raising interest rates. Amit made aggressive moves to prepare the company for leaner times, laying off 11% of employees. “We knew we had fat in the organization,” he says. While the company maintains sizable staff in Israel, San Francisco and Vancouver, when it started hiring again, it emphasized lower-cost locations like Tbilisi, Georgia. And Tipalti continued to grow–it now processes about $5 billion in monthly payments, up from $3 billion at the time of its 2021 fundraise. (The company says it retains 99% of its customers each year.) So what’s Tipalti worth now? In the summer of 2023, a Tipalti shareholder sold about $20 million worth of stock on the secondary market at a $4 billion valuation, according to Oren Zeev, a venture capitalist and Tipalti cofounder. In the fourth quarter of 2023, Capital Group, one of the largest mutual fund companies in the world, marked its shares at $3.7 billion. Now Caplight, a San Francisco startup that both tracks secondary-market trades of private tech companies and provides a venue to trade shares, estimates Tipalti’s value at just $3.1 billion–a number that also takes account of the stock slump of several of Tipalti’s competitors including publicly traded Bill, which is off 80% since its late 2021 peak. Caplight shared with Forbes its valuations for a long list of fintechs it tracks. The chart below shows its estimates, as of March 8, for 11 of them–all sizable startups where private trades and other information available within the past year provide a foundation for those valuations. Of course, these are still just estimates. As befits a burst bubble, some of the declines in value from their fundraising peak valuation are dramatic–an estimated 79% for Klarna and 74% for Chime. Many of the companies, which were all given a chance by Forbes to comment on these values, pushed back, and you can see their responses in the company write-ups at the bottom of this story.

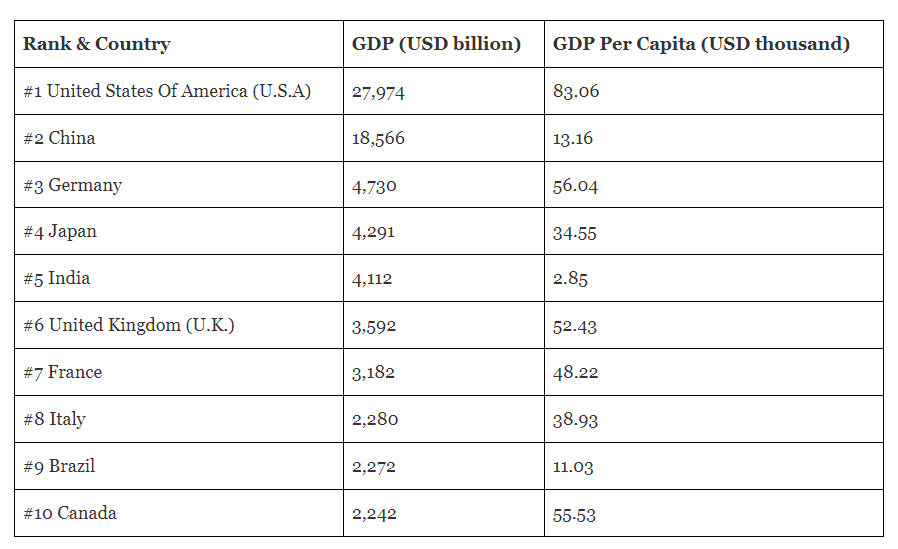

The United States of America, China, Japan, Germany, and India are the largest economies in the world in 2024, as per their GDP data. GDP serves as a key metric for assessing the magnitude of a nation's economy. The conventional approach for gauging a country's GDP involves the expenditure method, wherein the total is derived by aggregating expenditure on fresh consumer goods, new investments, government outlays, and the net value of exports. Below is a table of the top 10 largest economies/ richest countries in the world in 2024, sourced from IMF data (as of February 07, 2024). The US is world's largest economy with a GDP of $27.974 trillion (2024) and GDP per capita (USD thousand) of $83,060.  The United States of America :

The United States upholds its status as the major global economy and richest country, steadfastly preserving its pinnacle position from 1960 to 2023. Its economy boasts remarkable diversity, propelled by important sectors, including services, manufacturing, finance, and technology. The United States enjoys a substantial consumer market, fosters innovation and entrepreneurial spirit, possesses resilient infrastructure, and experiences advantageous business conditions. Source: https://www.forbesindia.com/article/explainers/top-10-largest-economies-in-the-world/86159/1

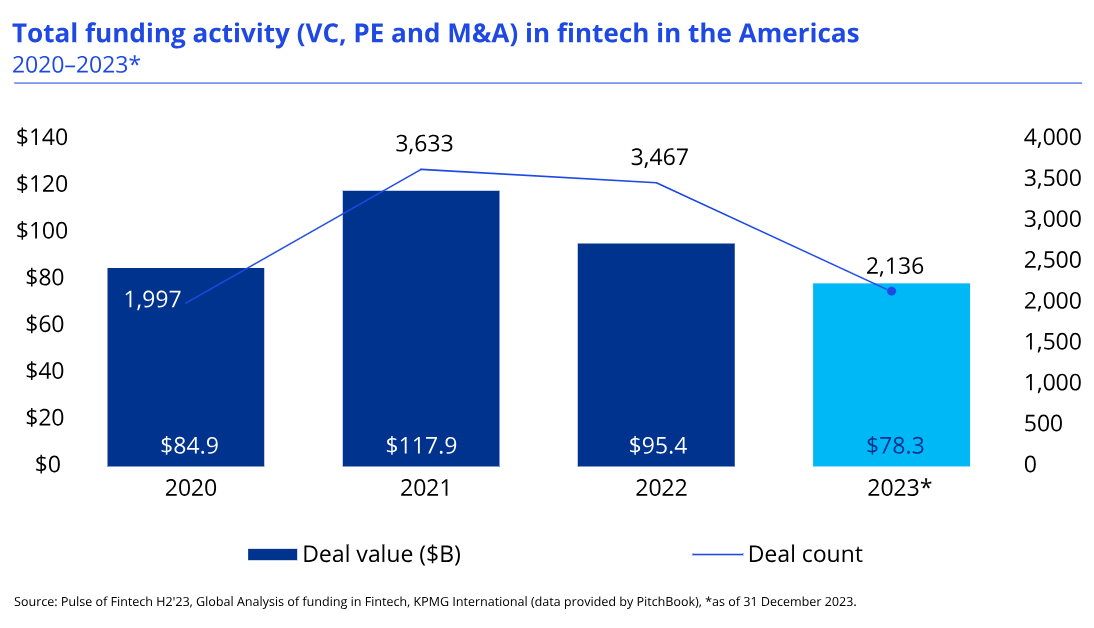

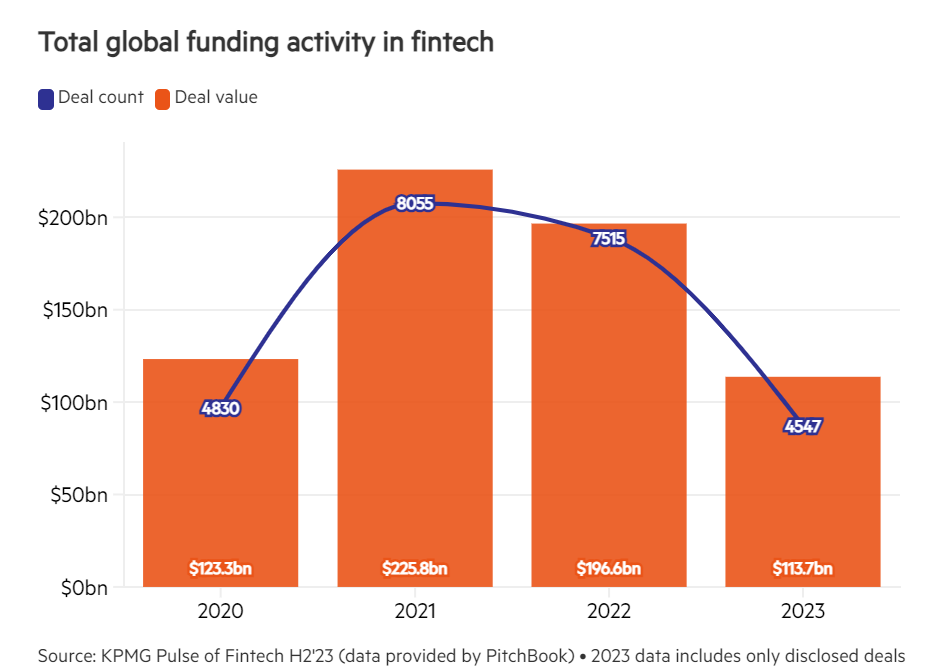

Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland) #FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com  Total fintech investment in the Americas reached an estimated $78.3bn with 2,136 deals in 2023. Total fintech investment in the Americas dropped from $95.4 billion in 2022 to $78.3 billion in 2023 as the number of fintech deals plummeted from 3,467 to 2,136. The US attracted the vast majority of fintech deals activity during the year, accounting for $73.5 billion of investment across 1,734 deals. The second half of 2023 was particularly soft for fintech deals activity in the Americas as investors enhanced their scrutiny of potential deals even further. During H2’23, the Americas attracted $38.4 billion of investment across 916 deals, of which the US accounted for $34.8 billion across 627 deals. The three largest deals in H2’23 occurred in the US, including the $11.7 billion acquisition of real estate data analytics company Black Knight by Intercontinental Exchange, the $10.5 billion acquisition of regtech and risk management software firm Adenza by Nasdaq, and the $1.2 billion buyout of wealth management firm Avantax by Cetera.  Global investment in fintech nosedived in 2023, plunging to a five-year low of $113.7bn from 4547 deals Global investment in fintech nosedived in 2023, plunging to a five-year low of $113.7bn from 4547 deals. This marked a 42 per cent decline from the $196.3bn reported in 2022 and represented the weakest result since 2017. Source: (1) https://kpmg.com/xx/en/home/insights/2024/02/pulse-of-fintech-h2-2023-americas.html and (2) https://www.thebanker.com/Global-fintech-investment-collapses-in-2023-1707725810

Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland) #FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com  UPDATE: 01 April 2024. The list of the top 10 US banks can be found here. At the start of 2023, the top 5 US banks by balance sheet were: JPMorgan Chase ($3.21tn), Bank of America ($2.41tn), Citigroup ($1.714tn), Wells Fargo & Co ($1.712tn) and U.S. Bancorp ($591bn).

The Federal Reserve has rolled out a list of top US banks by assets as at 31 December 2022. For decades, banks have been merging, partnering, and expanding—so much so that the top four banks accounted for 50% of all US banking assets last year. In addition to having more than a trillion dollars in consolidated domestic assets, JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo increased their tech spending to meet the growing demand for efficient mobile banking apps and compete with neobanks and other fintechs. The incumbents’ shift towards digital strategy gave them an edge among customers—from traditional to early adopters—regardless of their level of comfort with technology. This demonstrates that digital payment options are no longer complementary, but crucial in today’s mobile-first world. These are the top 10 banks in the US by assets, with key insights as to how they got there, where they plan to go in the future, and how smaller banks can stand out in a competitive industry. At the start of 2023, the 10 largest banks in the USA are:

Source: https://www.emarketer.com/insights/largest-banks-us-list/

Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland) #FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com  Fintech Ireland Map Supporter, Intersystems, has today released its research survey of over 500 senior decision-makers at fintechs across 12 countries, including the UK and Ireland, North and South America, and Australia and Southeast Asia.Data has Become the Biggest Technical Challenge for 81% of Fintechs Worldwide

Issues with data prevent fintechs from improving service offering and adopting next-gen technologies according to new survey of over 500 decision-makers ETON, UK., 26th January 2022 – Eighty-one percent of global fintechs cite data issues as the biggest technical challenge they face, with almost three-quarters (74%) of fintechs whose solutions are in the early adoption phase and almost all (85%) of those with an established offering or whose products have large scale adoption see it as their biggest technical challenge. According to research commissioned by InterSystems, a creative data technology provider dedicated to helping customers solve the most critical scalability, interoperability, and speed problems, these struggles are split between leveraging data for analytics, machine learning, and artificial intelligence (41%) and connecting to customers’ applications and data / legacy systems (40%). Security was also found to be a significant challenge for 40% of respondents, followed by cloud support / multi-cloud deployment and administration (39%). The survey of over 500 senior decision-makers at fintechs across 12 countries, including the UK and Ireland, North and South America, and Australia and Southeast Asia, found that cloud tops the list for over half (51%) of respondents adopting new technologies in the next 12 months. This is followed closely by plans to invest in data management technology (48%), artificial intelligence (AI) and machine learning (ML) (45%) and data fabric technology (42%). “While the majority of fintechs currently face significant data challenges, it’s encouraging to see many of them are looking to implement data management technologies like data fabrics to overcome them”, said Mike Hom, Head of Financial Services Solutions, InterSystems. This is an important step for both established and emerging fintechs, as getting their data in order will ensure any new data-related initiatives they undertake, such as implementing AI or ML, prove effective and worthwhile. By picking the right data management solutions, fintechs can also gain access to those more advanced technologies and analytics capabilities that are so desirable.” The levels of investment into these technologies do differ in relation to the maturity of the organisation, with the more established fintechs focusing more on data management (49%), cloud (54%) and data fabric initiatives (44%). Meanwhile, those fintechs whose offerings are still in the early adoption phase are more likely to prioritise investments in AI and ML (51%). This indicates that more established organisations are focused on overcoming the data issues they are facing before considering implementing new technologies like AI/ML, which rely on data. These investments are being driven by a number of different initiatives:

Rabih Ramadi, Head of Financial Services and Insurance at Unqork, an enterprise-grade no-code platform, commented, “Investing and integrating with the next generation data management technologies such as InterSystems is a top priority for us to ensure that our applications offer vital bidirectional, real-time data integration with our customers’ legacy systems. With such capabilities, data is no longer seen as a challenge but rather a critical differentiator empowering our customers to innovate faster to meet their business goals.” However, it was found that a number of fintechs still face barriers to implementing new technology, with a lack of flexibility within their current environment to integrate new technology (54%) and a lack of internal expertise / skills (51%) cited as the largest. Looking at their offering, 39% of fintechs surveyed offer a cloud-based managed service available in multiple public clouds and almost a quarter (23%) offer a hybrid application. This prevalence of cloud is despite 39% of respondents previously saying cloud support is one of their top technical challenges. This is a problem felt across the board from start-ups to established players, which could point to issues such as vendor lock-in, lack of real-time cloud availability and a shortage of expertise in security, cost-management, data-locality and integration of services. “While the complexity of cloud and its costs are major challenges for fintechs, especially as they grow, if they take the right approach to cloud deployments, these organisations can reap significant rewards and deliver those back to their end customers,” added Hom. “Boosting training and knowledge, along with building their offerings on cloud-first solutions that avoid vendor lock-in and which can be implemented within a hybrid environment will allow fintechs to increase agility, scalability, and security and ensure that their solutions appeal to a wider customer base.” About InterSystems Established in 1978, InterSystems is the leading provider of technology for critical data initiatives in the healthcare, higher education & research, finance, manufacturing, and supply chain sectors, including production applications at most of the top global banks. Its cloud-first data platforms solve interoperability, speed, and scalability problems for large organisations around the globe. InterSystems is committed to excellence through its award-winning, 24×7 support for customers and partners in more than 80 countries. Privately held and headquartered in Cambridge, Massachusetts, InterSystems has 25 offices worldwide. For more information, please visit InterSystems.com/Financial What: Fintech Ireland International Maps - Webinar (supported by US Fintech) When: Thursday 18 November 2021. 14:00-1530 Irish/UK time (09:00-1030 US Eastern Time). Where: Online Event Cost: Free Why: There are lots of US fintech doing business in Ireland. They are showcased on the Fintech Ireland International Map. If you are a US Fintech / US Techfin with a presence in Ireland, you can join the Maps by completing the Survey - Click Here. Details: Register - Click Here See the March 2021 edition of the Maps below or at https://fintechireland.com/fintech-ireland-map.html. November 2021 editions will be available to the public from 18th November 2021. Read more about the work of Fintech Ireland here - https://fintechireland.com  The registration platform for this event is now open to attend this joint event between Fintech Ireland, Choose New Jersey and New Jersey City University School of Business together with Tech United (New Jersey), Global Shares, Fenergo, Broadridge and SelectUSA (supported by Armstrong Teasdale).

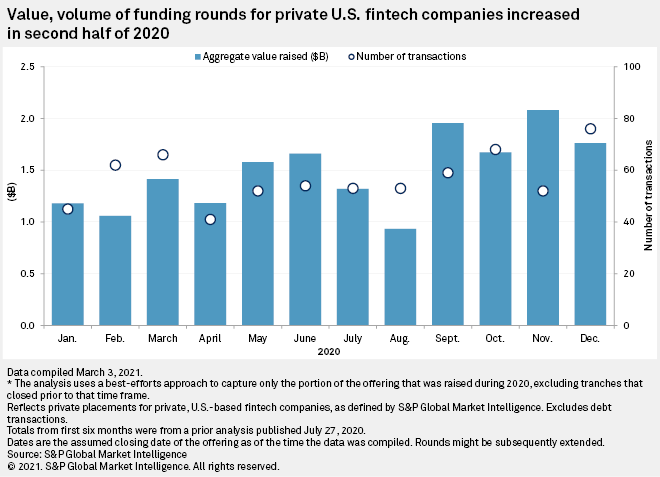

US Fintech and US TechFin are delighted to be supporting this event happening Wednesday 14th April 2021. 15:00-1630 Irish/UK time (10:00-1130 US Eastern Time)! REGISTER HERE. Join FinTech Ireland, Choose New Jersey and the New Jersey City University (NJCU) School of Business together with Tech United, Global Shares, Fenergo, Broadridge and SelectUSA (supported by Armstrong Teasdale) for a webinar on fintech trends and opportunities within Ireland and the U.S. State of New Jersey. Hear from New Jersey Governor Phil Murphy, business leaders and panel experts about economic synergies between New Jersey and Ireland and gain insight about the New Jersey’s innovation ecosystem and talent pool. Discover how New Jersey can provide Irish companies with the support, funding, and resources needed for successful investment in North America. What: Fintech Bridge - Ireland and New Jersey When: Wednesday 14th April 2021. 15:00-1630 Irish/UK time (10:00-1130 US Eastern Time). Where: Online Event Cost: Free Registration: https://fintechireland.com/events/fintech-bridge-ireland-new-jersey-tues-14th-april-2021  S&P Global Market IntelligenceU.S. fintech funding in 2020 outpaced 2019 in both amount raised and volume of transactions, despite — and in some ways due to — the COVID-19 pandemic. S&P Global Market Intelligence foresees another strong year in 2021, which has already burst out of the gates due to Robinhood Markets Inc.'s $3.4 billion raise amid the GameStop Corp. frenzy.

Though the virus wreaked economic havoc in 2020, interest rates remained relatively low, consumers embraced digital channels and the routes for venture capital firms to exit their investments, be it public offerings or M&A, remained open. Each of these factors likely contributed to the $17.8 billion that investors poured into private U.S. fintech companies in 2020, via 681 transactions, up from $14.8 billion and 539 transactions in 2019. While the fundraising situation appeared somewhat precarious in April 2020, with the volume of transactions falling about 38%, activity rebounded in subsequent months. Source: S&P Global Market Intelligence: https://www.spglobal.com/marketintelligence/en/news-insights/research/us-fintech-funding-still-going-strong-following-20-jump-in-2020  North America, and predominantly, the USA remains the No. 1 destination for Irish fintech expanding internationally according to leading Irish fintech network group, Fintech Ireland. The results were included in the webinar on 15th March on the Release of the Fintech Ireland Maps. This year, together with the usual updated Indigenous fintech map, the team released the inaugural international fintech map for Ireland with a host of US companies being identified. That explains why we support Fintech Ireland and perhaps why you should too. Read all about the event, watch the video and access the presentation slides at Fintech Ireland's Event page here. And take the time to read Sean Murray's, President and Chief Editor of deBanked, excellent and concise article on the event were he notes that "Though the Republic’s entire population (4.9M) is less than that of New York City (8.7M), it is home to nearly 250 indigenous fintech companies"   11th February 2021:

1) Remarks to attendees of the European Financial Forum in Ireland

The above remarks cover international financial services, brexit, fintech, payments, banking, the proposed Digital Euro, regtech, blockchain, digital assets, diversity & inclusion, monetary union Ireland's talented workforce, low corporate tax rate and export and inward investment opportunities. Did you know that the euro is the 2nd most used 'payments currency' globally? 2) Ireland's Minister of State for Financial Services, Credit Unions, and Insurance Seán Fleming TD launches the Ireland for Finance Action Plan for 2021. The Action Plan was announced during the Minister's speech at the European Financial Forum. Read more here New actions, include:

Check out this upcoming webinar featuring US TechFin Intersystems, co-hosting with Fintech Ireland on the topic of Big Data!

Fintech Future: Banking on Big Data “a 'data driven' approach is emerging across the financial sector affecting institutions business strategies, risk and operations with respective changes in the mind-set and culture still in progress” What: Fintech Future: Banking on Big Data (Fintech Ireland & Intersystems) When: Tuesday 19th January 2021 at 1400 Irish/UK time (0900 US Eastern Standard Time) Where: Online Event Cost: Free Registration: https://intersystems.com/uk/fintechirelandwebinar (or via https://fintechireland.com/events/the-future-of-fintech-banking-bigdata) Description: Fantastic response to and signups for the Fintech Ireland and InterSystems UKI upcoming co-hosted webinar on "The Future of Fintech: Banking on Big Data" with an expert panel of regulator and industry data experts who will discuss the growing importance of this area for TechFin, Fintech & FinServ. A 'data driven' approach is emerging across the financial sector affecting institutions business strategies, risk and operations with respective changes in the mind-set and culture still in progress. Speakers:

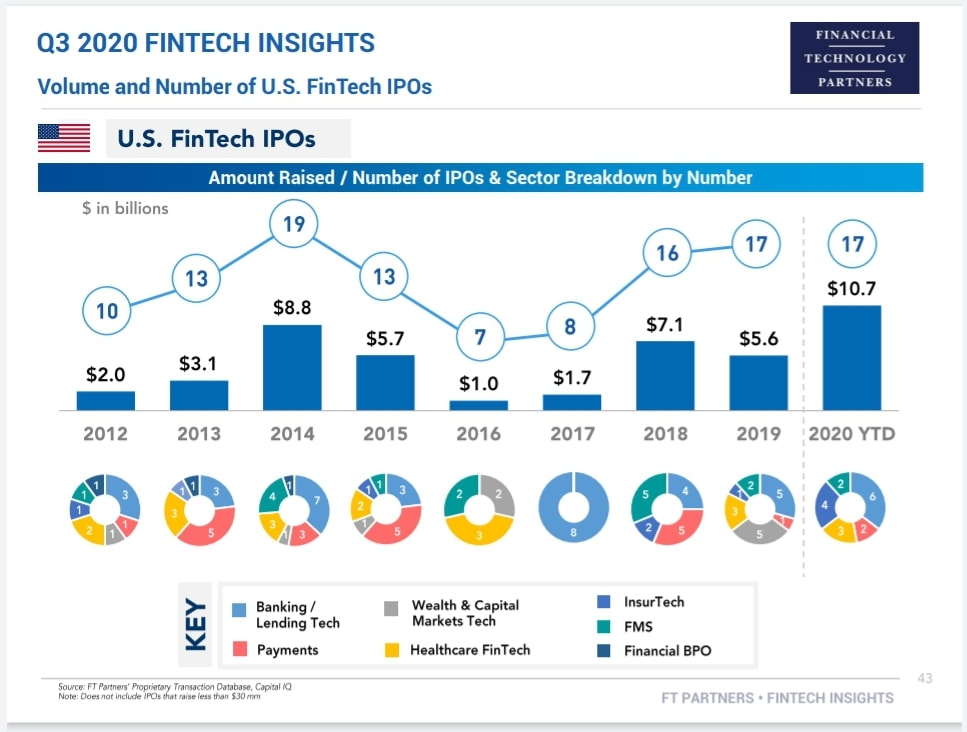

Thanks to Simon Cocking & the team at Irish Tech News for covering & publishing articles on the impact of big data & advanced analytics: * Leveraging Innovative Technology To Ensure Success For Ireland’s Fintech Sector - https://irishtechnews.ie/leveraging-innovative-technology-ireland-fintech/ * Fintech Future: Banking On Big Data - https://irishtechnews.ie/fintech-future-banking-on-big-data-webinar/  This blog is curated based on material published by FT Partners.

FT Partners Publishes Q3 2020 FinTech Insights The top 10 take-aways about Fintech in Q3 2020, according to FT Partners:

Read More: Note: FT Partners’ FinTech Insights Reports are published on a quarterly basis, along with a comprehensive year-end FinTech Almanac. All information included in the reports is sourced from FT Partners’ Proprietary Transaction Database, which is compiled by the FT Partners Research Team through primary research and data analysis.  We could not agree more, David! This article in Forbes neatly positions the TechFin v FinTech debate (if there is one at all) and why we are delighted to have USTechFin.com to complement US-Fintech.com. "it is the TechFins, not the FinTechs, who are the real challengers. "The TechFins, not the FinTechs, who are the real challengers." says David G.W. Birch, Contributor Fintech, Forbes.com who is a Fintech Author, advisor and global commentator on digital financial services. Other points to note:

Further reading: The Economist (“Plug and pay”, 21st November 2019)  As lawmakers working on a stimulus bill, US TechFin lenders have commenced lobbying the US government to part of the federal stimulus plan for businesses hurting from the coronavirus slowdown.

On Friday 19 March, in response to the COVID-19 economic crisis, Financial Innovation Now (FIN) called on Congress to help small businesses immediately by using alternative lenders to help distribute loans digitally. There is a concern that many small businesses will run out of working capital in less than three weeks. This concern is driven by (1) these businesses not being well served by traditional financial institutions and (2) will not benefit from existing federal small business loan programs soon enough. FIN sent a letter to Congress on Friday asking that its members be included in any emergency U.S. government funding. “Small businesses are not well served by traditional financial institutions, nor will existing federal small business loan programs deliver funds soon enough,” the letter reads. “Any federal small business loan program must leverage digital advances in the marketplace to ensure that stimulus can reach those business most in need.” wrote Brian Peters, FIN's Chief Executive. Mr Peters' letter adds that "FIN companies alone have made over $10 billion available in the past several years. Alternative online lenders have the reach, relationships, and digital capabilities to reach those businesses most vulnerable – right now." Source: hhttps://financialinnovationnow.org/news/ and https://www.cnbc.com/2020/03/23/tech-lenders-push-for-a-piece-of-the-coronavirus-bailout.html Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland) #FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com  Yesterday (23 March 2020) we reported that Revolut, one of Europe’s biggest fintech (financial technology) firms, has launched a “money management” product for children, which can be monitored by parents via the app.

Today Fintech Revolut announced that its financial app used by more than 10 million people worldwide, has landed in the United States. This development is owed to its partnership with Metropolitan Commercial Bank for the banking infrastructure — deposits are FDIC insured up to $250,000. Revolut is promising Americans that they can open a Revolut account in minutes, directly from their Android or iOS smartphone. Of course, like all those opening accounts, new American customers will need to provide some valid identification documentation. In just a few years, Revolut has managed to attract over 10 million customers by building a financial hub that lets you spend, send, receive and manage money from a single app. The company recently raised a $500 million funding round, valuing the company at $5.5 billion. Tens of thousands of U.S. customers have signed up to the waiting list and they’ll now be able to access all of Revolut’s core features. One of Revolut’s key features is that customers can convert from one currency to another based on interbank rate with a low fee — sometimes without any markup for popular currencies and small transactions (more details on foreign exchange fees here). Customers can hold foreign currencies in your Revolut account or send money to another Revolut user or a bank account in another country. Here's a list of what Revolut is promising:

Source: https://blog.revolut.com/revolut-launch-united-states/ and https://techcrunch.com/2020/03/24/revolut-launches-its-neobank-in-the-us/ Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland) #FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com  Revolut, one of Europe’s biggest fintech (financial technology) firms, has launched a “money management” product for children, which can be monitored by parents via the app.

The online-only bank, which claims more than 10 million users worldwide, announced Wednesday it was launching Revolut Junior, an app aimed at kids between the ages of 7 and 17. The accounts will come with their own bank card for the child to use. Revolut was founded in 2015 and has added features like cryptocurrency trading and savings products to its app over the years in an effort to become profitable. However, Revolut’s losses doubled in 2018 to £32.8 million ($42.4 million). Source: https://www.cnbc.com/2020/03/18/revolut-junior-british-challenger-bank-launches-accounts-for-children.html Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland) #FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com  In a continuing effort to encourage technological innovation in the banking sector, FDIC’s technology lab FDiTech has released “Conducting Business with Banks: A Guide for Third Parties” a guide to help Fintech companies partner with banks.

In its press release the FDIC says that:

The FDIC Chairman Jelena McWilliams says "The FDIC will continue to work with banks and fintechs to help them understand how they can effectively work together to serve our nation's depositors." FDIC established FDiTech in 2019 to collaborate with community banks on how to deploy technology in delivery channels and back office operations to better serve customers. FDiTech is working to encourage innovation and partnerships at community banks through engagement, technical assistance, tech sprints, and pilot programs. Source: https://www.fdic.gov/news/news/press/2020/pr20017.html Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland) #FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com  Stripe and Coinbase are regulated in Ireland to provide emoney services and Stripe, Coinbase, Robinhood, Plaid and Credit Karma are regulated in the United Kingdom.

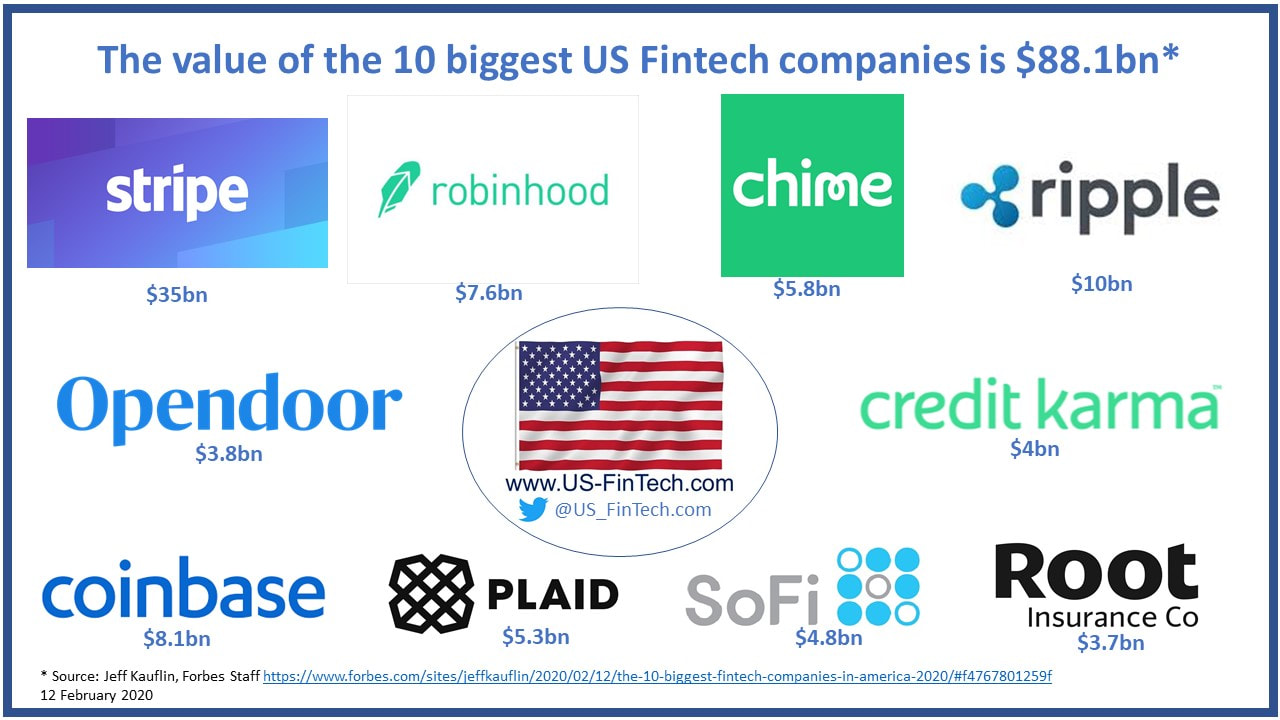

Who are "The 10 Biggest Fintech Companies In America 2020" according to Jeff Kauflin of Forbes? 1. Stripe - $35bn 2. Ripple - $10bn 3. Coinbase - $8.1bn 4. Robinhood - 7.6bn 5. Chime - 5.8bn 6. Plaid - $5.3bn 7. SoFi - $4.8bn 8. Credit Karma - $4bn 9. Opendoor - $3.8bn 10. Root Insurance - $3.7bn Source: https://www.forbes.com/sites/jeffkauflin/2020/02/12/the-10-biggest-fintech-companies-in-america-2020/#373c5fd81259. Consider following the author, Jeff Kauflin at https://twitter.com/JeffKauflin Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland) #FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com  The world’s biggest lender by market capitalisation is set to introduce savings and loans products using the Chase brand in the next few months, according to Sky News.

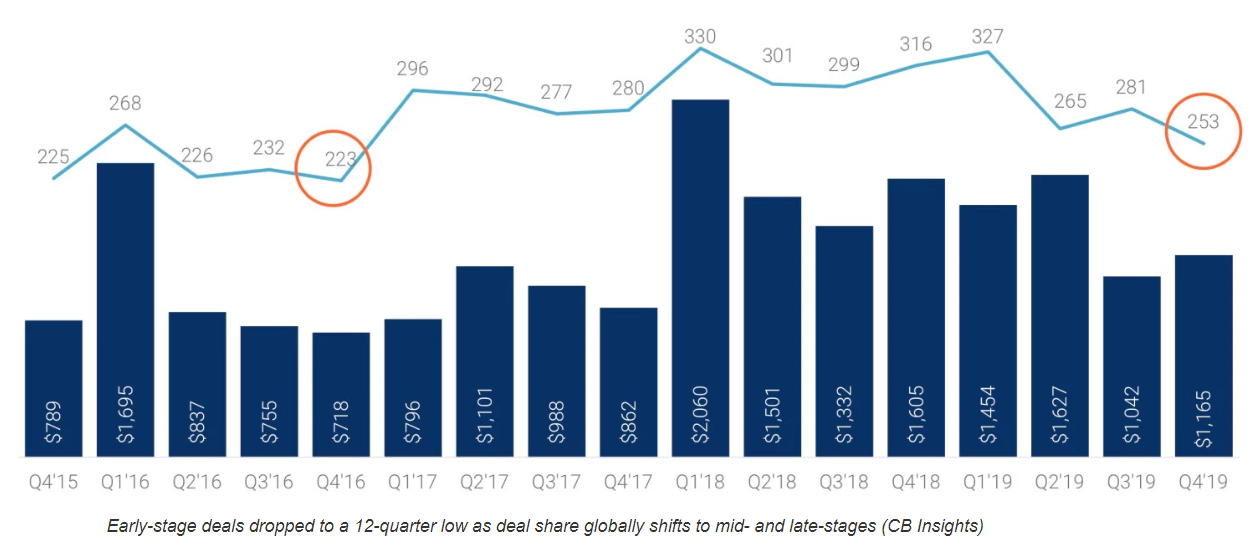

The New York-listed bank is due to hold an investor day next week and will set out growth strategy details. It is believed that the bank will launch a range of savings and loan products using the Chase brand in the UK in the next few months. This significant new entry into the UK consumer banking sector could spark a new price war among lenders already struggling to deal with a protracted period of ultra-low interest rates. Sources told Sky News that JPMorgan Chase has been in discussions with City and banking regulators about securing the necessary approvals to pave the way for the launch. It is understood the new service could launch as early as the second half 2020. The US-based bank reported in its fourth-quarter earnings last month that Chase had an average deposit base of $708bn (£540bn). Source: https://news.sky.com/story/jpmorgan-plots-launch-of-digital-consumer-bank-in-britain-11940211 Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland) #FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com UPDATE 1 January 2024: Total fintech investment in the Americas reached an estimated $78.3bn with 2,136 deals in 2023. See updated post here Below is out post of 22 February 2020   Great article by CB Insights. Reports that financial services startups raised less money in 2019 than they did in 2018 as VC firms looked to back late stage firms and focused on developing markets, a new report has revealed. CB Insights’ annual report found that fintech startups across the world raised $33.9 billion in total last year across 1,912 deals, down from $40.8 billion they picked up by participating in 2,049 deals the year before.

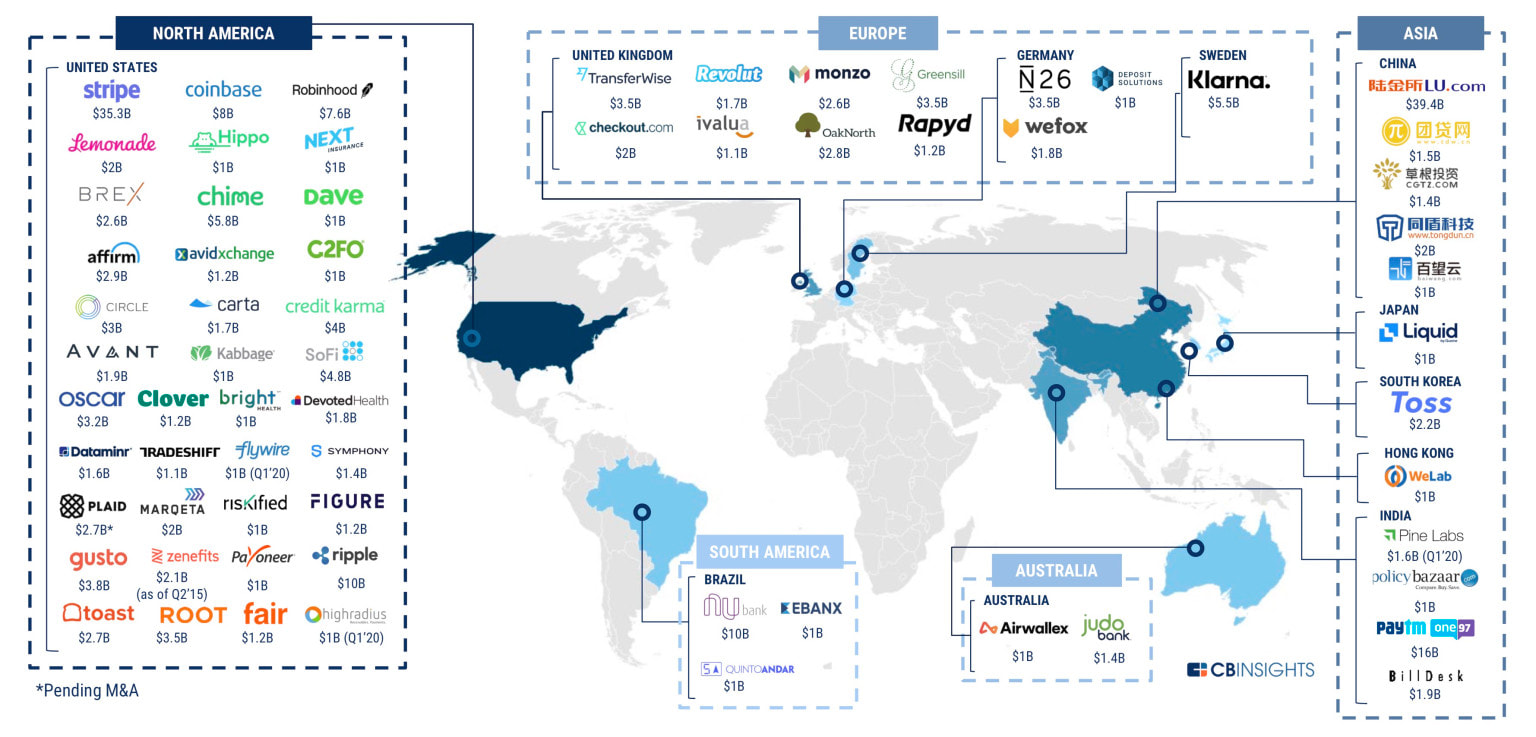

Image 1: In the North America box in the first image above, you will see those firms we wrote about in another post today on the Top Ten US Fintechs worth $88.1bn. Image 2: The bar chart above early-stage deals dropped to a 12-quarter low as deal share globally shifts to mid- and late-stages. The comprehensive report covers:

Source: https://www.cbinsights.com/research/report/venture-capital-q4-2019/ and https://techcrunch.com/2020/02/22/fintech-startups-raised-34b-in-2019/ Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland) #FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com  Varo Money, a mobile-only finance start-up, is a step closer to becoming a full-scale bank following the FDIC's approval of the fintech company’s national bank charter application.

This means Varo Money may now take customer deposits. Over the last number of years the US has seen many fintech and community bank partnerships where the likes of Varo, Chime, Robinhood and Square focus on customer interface apps leaving it to the banks that they partner with to hold customers’ money. Other examples of these types of partnerships include Apple and Goldman Sachs for the Apple Card and Google with Citi for a debit card. The deposits in the Varo arrangement are currently held by Bancorp. Those customer deposits will soon be transferred over to Varo subject to a few regulatory hurdles. Varo, valued at $417.8 million is backed by TPG and Warburg Pincus. It has someway to go to achieve the lofty valuations of newcomer US digital banks, such as Chime last valued at $5.8 billion. While non-US fintechs, such as Revolut and N26 are eyeing the US banking sector, none have progressed to an almost fully chartered bank status. Irish HQed fintech TransferMate partnered with Wells Fargo in 2019 to deliver "Global Invoice ConnectSM" which is used by US-based international businesses looking for more cost-effective solution for receiving payments from their global customers. TransferMate, while not a bank, is licensed across the US as a money service business, complementing its licensing and registration in Europe, Australia, Asia and the Middle-East. Other examples of fintech heading into banking territory include:

Source: https://www.cnbc.com/2020/02/11/start-up-bank-varo-gets-approval-to-become-a-full-scale-bank.html. Consider following the author Kate Rooney. https://www.independent.ie/business/irish/transfermate-seals-major-deal-with-us-giant-wells-fargo-38124846.html Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland) #FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com  16 January 2020: Peter Oakes, Founder of US Fintech (Fintech Ireland and Fintech UK) has been recognised as leading fintech expert by the prestigious Chambers & Partners’ 2020 for its Professional Advisers guide for FinTech – the premier ranking of professional advisers to the financial services industry.

Peter Oakes secured a nationwide Ireland Band 1 ranking – Chambers’ top-tier ranking – where it was noted that: Peter Oakes, who has vast international regulatory experience as a former director of the Central Bank of Ireland. A source says: ‘Peter is high-profile, he has very strong governance capabilities and is very good for a regulated FinTech company.' Peter Oakes is the Founder of US Fintech (www.us-fintech.com), as well as Fintech Ireland (www.fintechireland.com) and Fintech UK (www.fintechuk.com). Peter is a non-executive director of regulated fintech companies in the payments, e-money and MiFID sectors and is an adviser and mentor to fintech and regtech startups and scaleups. In Ireland he is a consultant to Clark Hill and in the UK he is a consultant to Kerman & Co, which is supporting the Fintech UK project. Learn more about Peter Oakes’s rankings in the Chambers FinTech guide here: https://chambers.com/department/peter-oakes-consulting-fintech-49:2743:114:1:23173986

Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland)

#FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com

UPDATED: 7 February 2024 (see post here)

The United States of America, China, Japan, Germany, and India are the largest economies in the world in 2024, as per their GDP data. GDP serves as a key metric for assessing the magnitude of a nation's economy. The conventional approach for gauging a country's GDP involves the expenditure method, wherein the total is derived by aggregating expenditure on fresh consumer goods, new investments, government outlays, and the net value of exports. Below is a table of the top 10 largest economies/ richest countries in the world in 2024, sourced from IMF data (as of February 07, 2024). The US is world's largest economy with a GDP of $27.974 trillion (2024) and GDP per capita (USD thousand) of $83,060

Below is our first post on the percentage share of the Global Economy held by the USA of 19 November 2024.

US has retained its position of being the world's largest economy with U.S. Nominal GDP: $21.44 tn; U.S. GDP (PPP): $21.44tn.

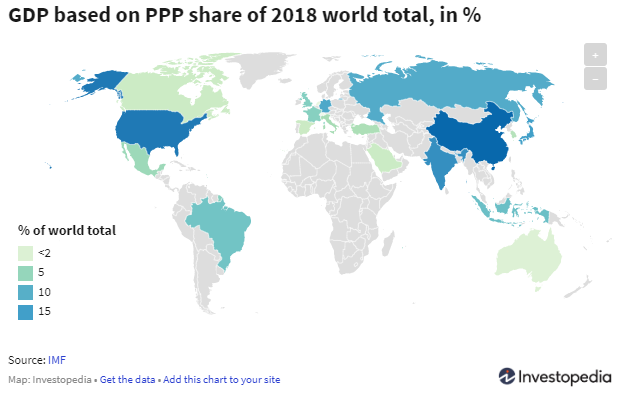

The US has been the world's largest economy since 1871. The size of the US economy is up from $20.58tn in 2018 (in nominal terms) and is forecast to hit $22.32 trillion during 2020. The US's economic superpower contributes almost a quarter of the global economy, backed by advanced infrastructure, technology, and an abundance of natural resources. Further evidence of the US economy's economic importance is noted in a previous US Fintech post which covers how the US biggest banks have grown substantially. The top 15 largest banks now hold a combined total of $13.7 trillion in assets. And the top 10 banks' share is approaching 80% of that figure, at $10 trillion. The US economy is projected to grow to $24.88 trillion by 2023, followed closely by China at $19.41tn. Countries by GDP

GDP based on PPP share of 2018 world total, in %

Source: https://www.investopedia.com/insights/worlds-top-economies/#1-united-states

Posted by Peter Oakes (www.peteroakes.com / Twitter @oakeslaw @US_Fintech @FintechUK_HQ @FintechIreland) #FintechUS #USFintech See also www.UKFintech.com www.FintechIreland.com |

AuthorPeter Oakes is the primary author and curator of this page. We welcome others, and you will be fully and fairly credited in your contribution. Archives

April 2024

Categories

All

Peter Oakes, Founder

|

RSS Feed

RSS Feed